2025-01-14 by Sue Hunt

Getting married is such an exciting time! Between the beautiful wedding, fun reception, and romantic honeymoon, there's a lot to celebrate. But it's also the perfect time to think about your future together and plan for the unexpected.

Estate planning might not be the first thing on your mind, but it's essential for everyone—whether you're young or old, married or single. It gives you peace of mind knowing that you and your loved ones are protected against life's surprises. Unfortunately, many couples spend more time planning their honeymoon than thinking about how to protect each other through estate planning.

Without an estate plan, things can get complicated if you become unable to manage your affairs due to illness or injury, or if you pass away. Here are some potential issues:

If you pass away without an estate plan, your spouse and loved ones will face additional challenges:

What Should You Do?

We invite you and your new spouse to call our office at 336-373-9877 to set up a meeting. We'll guide you through protecting each other, your loved ones, your pets, and your hard-earned assets. Let's make things easier for you and your families.

We look forward to hearing from you!

2025-02-04 by Sue Hunt

Valentine's Day spending totaled nearly $26 billion in 2024, including an all-time high of $6.4 billion spent on jewelry.[1] Yet many Americans report feeling disappointed that their partner did not do enough to celebrate Valentine's Day.[2]

More than 40 percent of US adults say they feel stressed about finding the perfect gift for loved ones.[3] About one-third plan to give a gift of experience this year instead of material possessions, marking a consumer shift toward gifts that are seen as more experiential and personalized than material items.[4]

While the gift of a qualified terminable interest property (QTIP) trust may not be the most romantic Valentine's Day gesture, it could prove to be more thoughtful, caring, and valuable than an off-the-shelf purchase.

What Is a QTIP Trust?

A QTIP trust is an irrevocable trust for married couples that offers a tax advantage for the trustmaker (the spouse who creates the trust) and financial security for the surviving spouse while preserving wealth for future generations. Here is how it works:

What Makes a QTIP Trust Different?

There are as many different types of trusts as there are flavors in a box of Valentine's Day chocolates. In a way that sets them apart from other trusts, QTIPs offer a unique balance between providing for a surviving spouse and maintaining trustmaker control over the trust's assets.

Customizing a QTIP Trust

One of the strengths of a QTIP trust lies in its flexibility. Some ways to customize a QTIP include the following:

Distributions of Principal

The trustmaker has almost unlimited leeway to dictate when and how the trustee can distribute principal to their spouse. For example, they can limit access to the principal for only health, education, maintenance, or support expenses (i.e., the HEMS standard). They can also give the trustee sole discretionary authority to distribute principal based on the spouse's needs. They can even prohibit spousal access to the principal altogether to preserve assets for remainder beneficiaries.

Spousal Control

Although the trustmaker has the final say on the ultimate distribution of assets when the surviving spouse passes, they can give the surviving spouse some degree of control using strategies such as a testamentary limited power of appointment,which lets the surviving spouse choose how the remaining trust assets are distributed upon their death among a defined group of beneficiaries predetermined by the trustmaker (e.g., children, grandchildren, other family members).

Why Use a QTIP Trust?

A QTIP trust can be an effective estate planning tool if you want to provide for your spouse after your death but ultimately limit the spouse's control over your assets and have your assets pass to different beneficiaries.

This arrangement may prove useful when you have children from a previous marriage, your spouse does not manage money wisely or has creditor issues, or there is some other unique family dynamic. A QTIP trust can also be part of a business succession strategy that ensures your spouse has an income stream from the business without being involved in running it.

This Valentine's Day, instead of the customary candy, cards, flowers, and jewelry, consider showing your love with the gift of a QTIP trust that lasts a lifetime—and, in many cases, even longer. Call our office at 336-373-9877 to schedule an appointment.

[1] Valentine's Day Shopping Statistics, CapitalOne Shopping (Dec. 18, 2024), https://capitaloneshopping.com/research/valentines-day-shopping-statistics/.

[2] Have you ever felt disappointed by a romantic partner not doing enough on Valentine's Day? YouGov (Jan. 18, 2021), https://today.yougov.com/topics/entertainment/survey-results/daily/2021/01/18/0f873/2.

[3] Niranjana Rajalakshmi, Why you're so stressed out about finding the perfect Valentine's Day gift, News, The Univ. of Arizona (Feb. 7, 2024), https://news.arizona.edu/news/why-youre-so-stressed-out-about-finding-perfect-valentines-day-gift.

[4] Consumers Plan to Increase Valentine's Day Spending to Nearly $26 Billion, Nat'l Retail Fed. (Jan. 24, 2024), https://nrf.com/media-center/press-releases/consumers-plan-increase-valentines-day-spending-nearly-26-billion.

2024-04-08 by Sue Hunt

As a parent, you are responsible for the care of your minor child. In most circumstances, this means getting them up for school, making sure they are fed, and providing for other basic needs. However, what would happen if you and your child's other parent were unable to care for them?

It is important to note that if something were to happen to you, your child's other parent is most likely going to have full authority and custody of your child, unless there is some other reason why they would not have this authority. So in most cases, estate planning is going to help develop a plan for protecting your child in the event that neither parent is able to care for them.

What If You Die?

When it comes to planning for the unexpected, many parents are familiar with the concept of naming a guardian to take care of their minor children in the event both parents die. This is an important step toward ensuring that your child's future is secure.

Without an Estate Plan

If you and your child's other parent die without officially nominating a guardian to care for your child, a judge will have to make a guardianship decision. The judge will refer to state law, which will provide a list of people in order of priority who can be named as the child's guardian—usually family members. The judge will then have a short period of time to gather information and determine who will be entrusted to raise your child. Due to the time constraints and limited information, it is impossible for the judge to understand all of the nuances of your family circumstances. However, the judge will have to choose someone based on their best judgment. In the end, the judge may end up choosing someone you would never have wanted to raise your child to act as your child's guardian until they are 18 years old.

With an Estate Plan

By proactively planning, you can take back control and nominate the person you want to raise your child in the event you and the child's other parent are unable to care for them. Although you are only able to make a nomination, your choice can hold a great deal of weight when the judge has to decide on an appropriate guardian. The most common place for parents to make this nomination is in their last will and testament. This document becomes effective at your death and also explains your wishes about what will happen to your accounts and property. Depending on your state law, there may be another way to nominate a guardian. Some states recognize a separate document in which you can nominate a guardian, and that document is then referenced in your will. Some people prefer this approach because it is easier to change the separate document as opposed to changing your will if you want to choose a different guardian or backup guardians.

What If You Are Alive but Cannot Manage Your Own Affairs?

Although most of the emphasis is on naming a guardian for when both parents are dead, there may be instances in which you need someone to have the authority to make decisions for your child while you are alive but unable to make them yourself.

Without an Estate Plan

Not having an incapacity plan in place that includes guardianship nominations means that a judge will have to make this judgment call on their own with no input from you (similar to the determination of a guardian if you die without a plan in place).

With an Estate Plan

A comprehensive estate plan can also include a nomination of a guardian in the event you and the child's other parent are incapacitated (unable to manage your own affairs). Although you are technically alive, if you cannot manage your own affairs, there is no way that you will be able to care for your minor child. This is another reason why having a separate document for nominating a guardian (as described above) may be preferable to nominating guardians directly in a last will and testament. Because a last will and testament is only effective at your death, a nomination for a guardian in your will may not be effective when you are still living. However, a nomination in a separate document that anticipates the possibility that you may be alive and unable to care for your child can provide great assistance to the judge when evaluating a guardian. Depending on the nature of your incapacity, this guardian may only be needed temporarily, with you assuming full responsibility for your child upon regaining the ability to make decisions for yourself.

What If You Are Just Out of Town?

Sometimes, you travel without your child and will have to leave them in the care of someone temporarily. While you of course hope that nothing will go wrong while you are away, it is better to be safe than sorry.

Without an Estate Plan

Without the proper documentation, there may be delays in caring for your child if your child were to get hurt or need permission for a school event while you are out of town. The hospital or school may try to reach you by phone in order to get your permission to treat them or allow them to attend a school event. Depending on the nature of your trip, getting a hold of you may not be easy (e.g., if you are on a cruise ship with little access to phone or email). Ultimately, your child will likely be treated medically, but the chosen caregiver may encounter additional roadblocks trying to obtain medical services for your child, and they may not be able to make critical medical decisions when needed.

With an Estate Plan

Most states recognize a document that allows you to delegate your authority to make decisions on behalf of your child to another person during your lifetime. You still maintain the ability to make decisions for your child, but you empower another person to have this authority in the event you are out of town or cannot get to the hospital immediately. This document allows your chosen caregiver to make most decisions on behalf of your child, except for consenting to the adoption or marriage of your child. The name of this document will vary depending on your state and is usually effective for six months to a year, subject to state law. Because this document is only effective for a certain period of time, it is important that you touch base with us to have new documents prepared so that your child is always protected.

We Are Here to Protect You and Your Children

Being a parent is a full-time job. We want to make sure that regardless of what life throws at you, you and your child are cared for. Give us a call to learn more about how we can ensure that the right people are making decisions for your child when you cannot.

2022-07-25 by Sasha Hartzell

Despite the fact that it happens to every single one of us and is as every bit as natural as birth, very few among us are properly prepared for death—whether our own death or the death of a loved one.

Yet the pandemic might be changing this.

According to Census figures, the pandemic caused the U.S. death rate to spike by nearly 20% between 2019 and 2020, the largest increase in American mortality in 100 years. More than two years and 1 million deaths later, it's more clear than ever that death is not only ever-present, but a central and inevitable part of all our lives.

Graph from the United States Census BureauSome in the end-of-life industry believe that the pandemic's massive loss of life has created an opportunity to transform the way we interact with death, grief, and all of the other issues that arise with the loss of a loved one. Seizing the moment, one startup recently launched Empathy, an AI-based platform designed to help families navigate the death of a loved one. "We're on a mission to change the way the world deals with loss," reads Empathy's 'About Us' page. The company's CEA and Co-Founder, Ron Gura echoes this sentiment:

"For far too many, COVID-19 has been a terrible reminder that death and loss are all around us. But it also represents an opportunity to shift public perception, to bring a topic that has been for far too long shrouded in darkness into the light of day, where we can fully examine it and figure out how best to help those who have to shoulder its burdens."

- Ron Gura, Co-Founder of Empathy

The death of a loved one generates a cascade of emotional, logistical, and financial challenges for those left behind. To further shed light on just how vastly unprepared most of us are when dealing with death, in March 2022 Empathy released its first-ever Cost of Dying Report. In partnership with Goldman Sachs, Empathy's report surveyed more than 2,000 Americans—each of whom had lost a loved one in the last five years—to get a clearer picture of dying's true cost to families.

The report looked not only at the financial burden dying brings, but also at the cost in time, stress, harmed productivity, and strained interpersonal bonds. Complete with insights from advisors, partners, and experts in bereavement, the Cost of Dying Report "bust open the taboo that has for too long kept it out of the public consciousness," said Gula.

Empathy found that the average total bill of death is $12,702. The average cost of a funeral was $7,267—according to the National Funeral Directors Association, that cost has risen 7.6% in the last 5 years. On top of the funeral, families paid an average of $5,846 to hire additional professionals such as lawyers, financial advisors, therapists, and realtors.

Excerpt from The Cost of Dying Report by Empathy

Excerpt from The Cost of Dying Report by Empathy

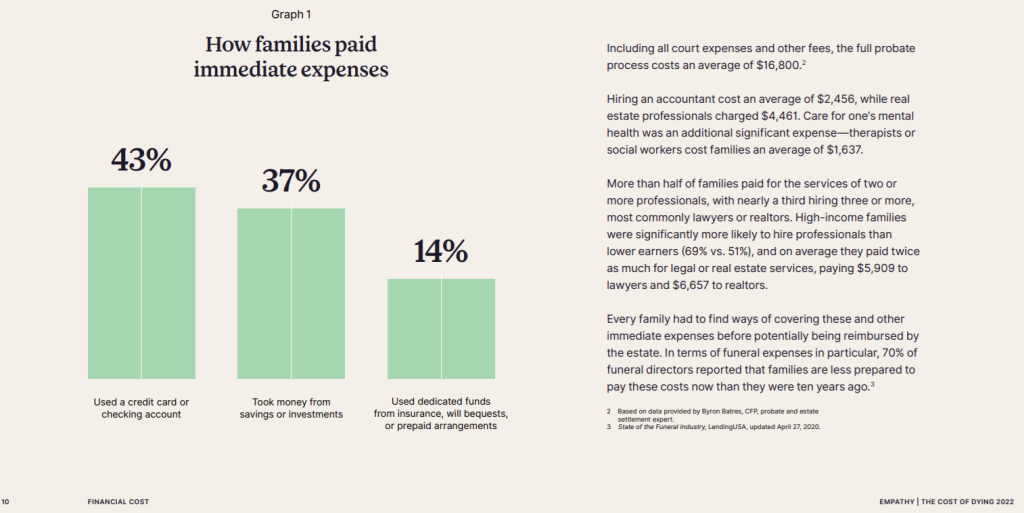

The average cost of lawyers fee's following the death of a loved one was $3,910. This amount, however, is nearly doubled for estates that required the court process of probate, as was the case for one-third of families surveyed; the average total cost to complete probate for the families surveyed was $16,800.

Beyond the purely financial, The Cost of Dying Report found that families spent 13-20 months completing end-of-life tasks for their deceased loved ones. Study participants clocked an average of 420 hours of work to handle an estate with around five phone calls a week (26 hours per month on the phone!) The majority of families also said it took longer to much longer than expected to wrap up all of the necessary tasks.

In the words of contributing attorney Avi Z. Kestenbaum, "every estate is settled eventually. Even the most complex one. But it is very often a long road to get there—and if you think you know how long, you probably don't."

So how do families cover all of these expenses? Unfortunately, the report found that only one in seven families had the costs associated with their loved ones' death prepaid, or were able to use inherited funds. Additionally, more than 50% of families had to deal with estates that included debt. To foot the bill for these expenses, 36.1% of respondents used their own savings or investments, while 42.4% used their checking accounts or credit cards.

For most families, the financial costs associated with loss were exacerbated by a lack of information about exactly how much money they should expect to spend, according to physician Shoshana Ungerleider, MD, in the report's section on death's financial cost. Compounding that stress, Ungerleider says, was the families' fear of making a mistake that will make their financial burden even worse.

"A majority of families find themselves unprepared for and under-informed about the real financial costs of death, with few available resources for finding out," writes Ungerleider. "They can spend months or years terrified that a wrong move will wipe out their inheritance or even their own savings."

As an example of what such a mistake might look like, Ungerleider notes that a lack of proper estate planning can lead to the deceased's home being seized after death for Medicaid Recovery, even if the family member who was their primary caregiver is still living in the home.

Fortunately, there are ways you can dramatically reduce the financial, logistical, and emotional burden for your loved ones upon your death. There are strategies to help your family to avoid the time, expense, and emotional burden associated with probate, such as by placing assets in a properly created and maintained revocable living trust. We also offer planning strategies that can help you and/or your senior parents qualify for Medicaid and other benefits, without putting the family home or other assets at risk.

Our end-of-life planning also includes asset protection, avoiding family conflict, funding long-term care, and estate tax mitigation, just to name a few. Sit down with us for a Family Wealth Planning Session to find the most effective and affordable planning solutions for you and your family.

The more you prepare for your own eventual death and learn about the process, the more support you can offer friends and family members who have recently lost a loved one. As Kestenbaum notes, "as a society, then, we can be much more aware not only of the stress that our bereaved friends, neighbors, coworkers, or employees are under, but also understand that the pressure will persist for a very long time. So even one year later, try to ask: How are you? Is there anything I can do to help? That will be very meaningful."

2026-04-10 by Julia Walker

Do I Need Long-Term Care Insurance and How Does It Work?

Policy experts and families alike have long noted that the United States lacks a comprehensive public system for long-term care.

Medicare generally does not cover these services, and while Medicaid can help, it is available only to people with very limited assets, often requiring a spend-down that can leave little or nothing for loved ones.

Private long-term care insurance (LTCI) offers a potential solution, but the market is more exclusive than it once was. The policies still available today are typically designed for relatively healthy people who can afford higher premiums.

In recent years, interest in the LTCI market has grown again, thanks in part to hybrid life insurance/LTC products. While LTCI is not right for everyone, both traditional and hybrid policies can play a useful role in protecting assets and supporting long-term care strategies.

What LTCI Is—and Is Not

KFF Health News and the New York Times recently published a series explaining why “few can afford to grow old” and many Americans are “dying broke” due to high long-term care costs and no universal public care system.[1]

Given this reality, a private LTCI policy may seem like a no-brainer. Yet the contraction of the LTCI market over the past few decades shows that this is a limited tool with a small target audience.

Around 70 percent of people aged 65 and older will need long-term care services during their lifetime, but fewer than 5 percent of Americans aged 50 and older own a long-term care policy.[2]

LTCI emerged in the 1970s and 1980s as a mass-market product, similar to life insurance but specifically designed to cover services that standard health insurance and Medicare typically do not pay for. It typically covers the following services:

● In-home care. Assistance with daily activities while staying at home

● Assisted living facilities. Supportive housing with care services

● Memory care. Specialized care for people with Alzheimer’s or other memory-related conditions

● Skilled nursing or nursing homes. Long-term skilled care in a facility with professional medical support

LTCI generally does not cover the following services:

● Short-term medical care that Medicare already pays for

● Care that does not meet policy requirements (Most policies only pay when you have significant cognitive impairment or cannot perform at least two activities of daily living, such as bathing or getting dressed.)

● Informal care by family or friends unless it meets the policy’s rules for coverage

What Else to Know About LTCI: Pricing, Options, and Fit

Why are more Americans not purchasing long-term care insurance? Let’s start with the benefits. Here is what LTCI can do:

● Provide dedicated funds for care

● Preserve assets for heirs

● Offer flexibility in choosing where and how care is provided

● Reduce reliance on family caregivers and Medicaid planning, including having to spend down savings

● Support spousal planning

But LTCI is far from a perfect solution and is not one-size-fits-all. These are some important factors to consider:

● Hybrid life/LTC products are growing in popularity,[3] combining long-term care coverage with a death benefit. They may be especially appealing to younger buyers or sandwich-generation families.[4]

● Some policies (especially older or narrowly designed ones) may not pay for all the care you assume is covered,[5] leading to substantial out-of-pocket costs.

● Modern policies often have stricter health requirements and more conservative pricing.

● A policy for a 55-year-old single man averages roughly $950 per year and about $1,500 for a single woman. A married couple of the same age purchasing coverage together may pay around $2,080 annually, with higher premiums for inflation protection, according to the American Association for Long-Term Care Insurance.[6]

● Plan features that affect pricing include age at the time of purchase, medical history and current health, daily or monthly benefit amounts, benefit duration, inflation protection, and waiting periods.[7]

With these factors in mind, LTCI may be worth considering in the following circumstances:

● You have meaningful assets at risk and want to reduce the possibility of care costs wiping out your savings.

● You want to preserve a legacy rather than using those assets for self-funded care.

● You want to protect a spouse’s financial stability if your partner requires care.

● You want to reduce the risk that care expenses will disrupt investments or other financial goals.

● You are healthy enough to qualify and can afford to pay premiums over the long term.

LTCI may not be a good fit in the following circumstances:

● You have limited cash or income flexibility, and premiums would stretch your budget or make other financial goals harder to achieve.

● You expect to rely primarily on public benefits; if you are planning for Medicaid to cover your care, LTCI may not be necessary.

● You have already arranged savings or trusts to cover care.

● You face health issues that may make it difficult or expensive to qualify for coverage.

● You are unwilling to commit to long-term premium obligations, preferring financial flexibility.

Whether LTCI is right for you comes down to a personalized analysis. The need for long-term care is becoming more common among aging Americans. However, a dedicated care policy is just one tool within LTC planning and the larger planning picture. You should evaluate its fit alongside your legal documents, insurance coverage, and financial goals so that long-term care—if it becomes necessary—does not dictate the choices available to you and your family.

[1] Dying Broke: A KFF Health News–New York Times Project, KFF Health News (Nov. 14–Dec. 15, 2023), https://kffhealthnews.org/dying-broke.

[2] Janet Weiner, Reforming Long-Term Care Policy: Lessons from the Past, Imperatives for the Future, Penn LDI (Dec. 4, 2025), https://ldi.upenn.edu/our-work/research-updates/reforming-long-term-care-policy.

[3] Is Life Insurance the Answer to the Growing Long-Term Care Need in the U.S.?, LIMRA (Aug. 28, 2025), https://www.limra.com/en/newsroom/industry-trends/2025/is-life-insurance-the-answer-to-the-growing-long-term-care-need-in-the-u.s.

[4] The Sandwich Generation: Balancing Care for Parents & Children, Caregiver Action Network, https://www.caregiveraction.org/sandwich-generation (last visited Mar. 31, 2026).

[5] Reed Abelson & Jordan Rau, Dying Broke: A KFF Health News–New York Times Project: Facing Financial Ruin as Costs Soar for Elder Care, KFF Health News (Nov. 14, 2023), https://kffhealthnews.org/news/article/dying-broke-facing-financial-ruin-as-costs-soar-for-elder-care.

[6] 2025 Long-Term Care Insurance Facts - Prices - Data - Statistics - 2025 Report, Am. Ass’n for Long-Term Care Ins., https://www.aaltci.org/long-term-care-insurance/learning-center/ltcfacts-2025.php (last visited Mar. 31, 2026).

[7] What Features of Long-Term Care Policies Should I Focus On?, Ins. Info. Inst., https://www.iii.org/article/what-features-long-term-care-policies-should-i-focus (last visited Mar. 31, 2026).